Companies that offer subscription-based products are well aware of the common reasons for customer churn. The product isn’t a great fit, competitors offer something better, or customers are tightening their belts and spending less. Whether a SaaS company, e-commerce, or another type of subscription service, it’s a natural phenomenon that customers opt to cancel.

But what if those customers didn’t intend to discontinue their subscriptions? “Accidental churn” happens when subscriptions are interrupted by payment failures. While some are avoidable, like proactively reaching out to a customer before a credit card expires, other recurring payments failures are driven by more complex, data-related issues. And these can make up anywhere from 10 – 25% of a company’s total revenue.

Not only is this problem pervasive, it is hard to tackle. Yet since the impacted customers don’t intend to cancel, it’s also a huge opportunity for companies to reduce churn — if they’re able to address the underlying causes.

The Core Challenge Behind Recurring Payments Failures

While subscription products and services have been trending for years, the underlying infrastructure to support such payments hasn’t kept up. The banking industry as a whole isn’t overly motivated to change, especially when the payment method of “walk into a store and swipe a credit card” worked for decades.

But subscriptions have been on the rise, consistently expanding five-to-eight times faster than traditional businesses, according to industry research. The pandemic accelerated this trend even more, especially in the technology industry, with companies offering flexible options and quickly pivoting to new product offerings and pricing bundles. The payments infrastructure hasn’t been equipped to handle online payments, often originating around the globe.

Each new subscription brings the risk of payment failures. Failed payments happen when a legitimate payment is declined by the payment network, a problem that can climb into millions of dollars as a company’s revenue increases.

The Ripple Effects of Failed Subscription Payments

The biggest difference between a one-time payment and recurring payments is that a customer can tell if an on-the-spot payment fails. The transaction is declined and the customer either tries again or gives up.

With subscription payments, a card processed correctly one month might fail the next month — and the customer isn’t even aware of the failure. And due to the number of ways that payments can fail, this creates headaches for teams across the company that have to deal with the issues.

- Customer service teams have to handle inquiries from confused customers

- E-commerce products can’t ship until payment is received, leading to supply issues

- The customer simply moves on and doesn’t correct the failed payment

- Customer acquisition costs increase because companies invest additional resources to acquire new customers to compensate for lost revenue

- Customer lifetime value decreases as their subscription is ended prematurely

Perhaps the hardest pill to swallow is the fact that were it not for the failed payments, the customer wouldn’t have churned. While companies can try to process the payment again, if the issue can’t be resolved, the risk is that the customer won’t bother trying another payment method. And then revenue is lost. The customer’s trust with the company is entirely broken and they will not come back.

4 Reasons for Recurring Payments Failures

Some payment failure reasons will always be outside of a company’s control, such as a stolen card. All the reminders in the world may never bring that customer back.

But there are other reasons for recurring payments failures that don’t involve customer interactions. Even though payments are processed in half a second, a data exchange happens in the background that can break down in several different ways. Think of a game of telephone: the message sent at the beginning can get lost in translation. And if that happens, a payment failure can occur.

The reasons payments can fail are interrelated, but they’re rooted in data communication: how information is passed during that fraction of a second when the payment is being processed.

1. Transaction Data Points

Every transaction has over one hundred data points that can be sent, such as the card expiration date and the zip code. The data points are sent to the processor, the processor sends the data to the payments network and the card issuer approves or declines the transaction, then the information is sent back.

When failures occur, it isn’t necessarily due to a lack of data. But the right data has to be sent to the downstream bank and meet that bank’s standards in order to be approved. Processors have to know whether or not to send a zip code, for example, along with other data points.

2. Inconsistent Error Codes

Every time a payment fails, an error code is returned. But even with more than two thousand unique error codes, there is no regulatory oversight or audit process that oversees how the error codes are returned. As a result, there are huge inconsistencies.

A company could submit a payment today and again in two days. Both payments are declined, but different error codes are returned — even with the exact same product and exact same price. The inconsistency makes the problem challenging for payments teams that try to address error codes so that fewer payments are returned. It’s hard to know what to address if it’s unclear what you’re chasing.

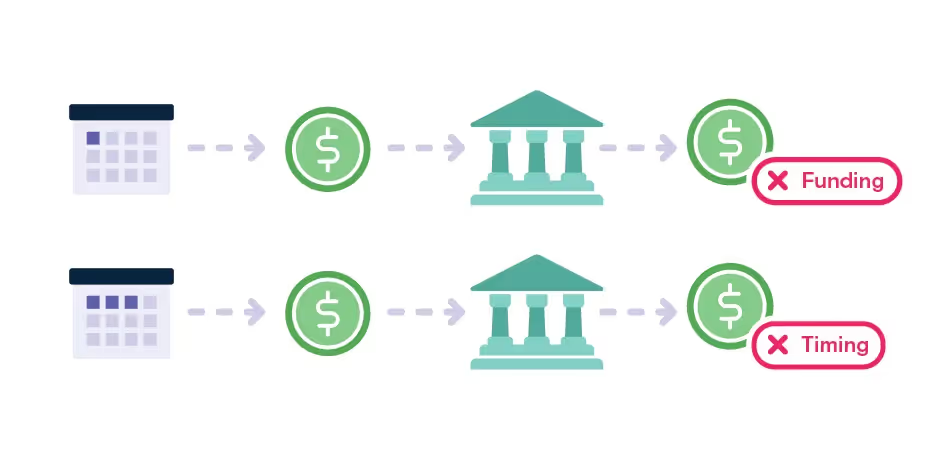

3. Payments Timing

Transactions run on a debit card do run the risk of insufficient funds. In a payment environment of the past, running transactions on a certain day of the week (like Fridays, when people are paid) could increase the possibility of successful payment. But in today’s world, people are paid at different intervals or even have earned wage access, where they can access their paychecks as money is accrued. Companies that have global customers are also dealing with multiple time zones. “Fridays at 8:00 am” don’t catch payday in the customers’ bank accounts the way they used to and companies have to figure out how to optimize payment timing.

4. Global Regulations

Not only do companies need to worry about how data is sent, but in a global economy, they also need to be concerned with the laws in different countries. And those laws, such as privacy laws, are constantly changing. For example, privacy laws in the US are not the same as privacy laws in Europe, so the same transaction might clear in the US but fail in Europe.

Issuing banks can change their standards rapidly to accommodate regulatory changes. It’s a dynamic problem that companies have to continually address in order to ensure payments continue to process correctly.

Ways to Recover Failed Payments

As a good business practice, but especially in a tight economy, companies should look to be smarter with their money and that includes examining failed payments. By narrowing down the problems, companies can reduce accidental churn.

- Customer support can alert customers and prompt them to change the card used

- Technology can assist with global regulatory changes and requirements

- Payment retries can resubmit payments on a different time and day

- Machine learning can optimize for payment processing

Each of these recoveries may chisel away at the 10 – 25% of the company’s revenue lost to accidental churn. Payment retries are often the most successful, with the standard being to batch-process transactions a few days later (and then again a few days after that if they fail again). That’s certainly the easiest for internal teams that are trying to “add logic” to their payments systems and address the payments failures.

Machine learning technology can take this a step further and optimize for individual transactions, rather than operating in large batches. By learning from payment failures over time, ML can process each transaction based on time zones, location, and other factors that cause payments to fail.

Improve Revenue With Failed Payments Recovery

Since engaging with customers will only go so far, companies should be looking hard at how technology can assist with failed payments. In addition to the revenue lost overall, each retried attempt to collect payment is time lost: days between when your company should have had the revenue and when it is actually received. And, as the saying goes, time is money.

Even though recurring payments failures are caused by separate, yet interrelated, issues, companies can still strive to prevent payment failures and optimize payment recoveries. By doing this, they can improve one of the top metrics for any subscription business: retention.

Butter’s machine learning technology helps companies recover payment failures. Contact us to learn more.

.png)

.png)

-min.svg.png)

-min.svg%20fill.png)